The Hidden Reason Some Fund Administrators Cost Twice As Much

March 18, 2026

Most fund managers have never spent much time thinking about the economics of fund administration.

For years, there was little reason to. Capital was flowing, margins were healthy, and the operational stack around a fund was rarely where managers looked for efficiencies. Administrators were chosen based on reputation, familiarity, or simply what investors expected to see on the service provider list.

We're entering a very different environment.

AI is beginning to reshape how operational work gets done. Fundraising has become harder. Managers are feeling pressure across their cost structures. In that environment, it becomes reasonable to revisit some long-standing assumptions.

One of those assumptions is fund administration.

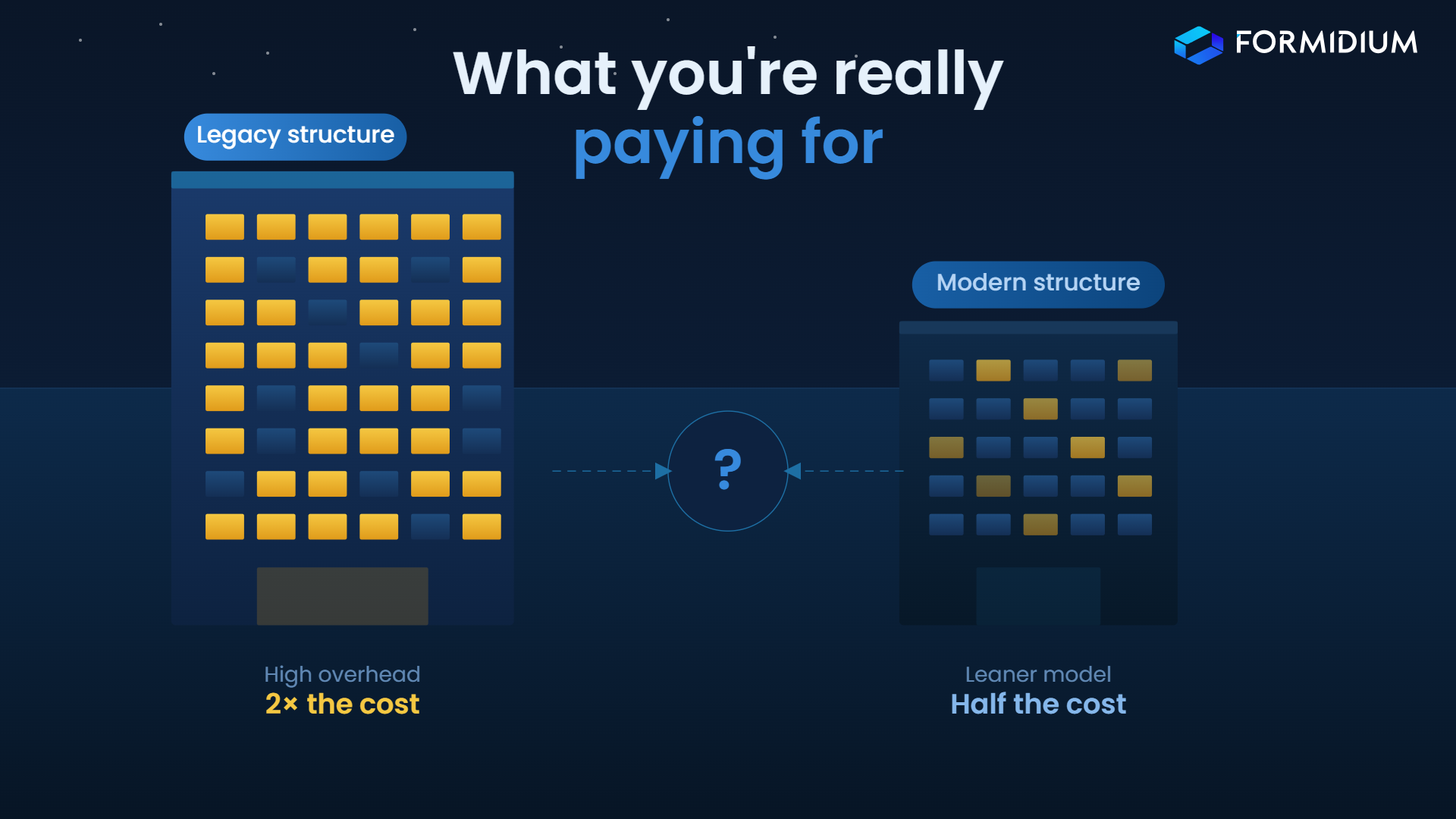

Two administrators can appear to offer essentially the same service, fund accounting, investor reporting, financial statements, tax support, yet one may cost dramatically more than the other. In some cases, the difference is two times the price.

That raises a simple question that surprisingly few managers have asked:

If accounting is accounting, why do some administrators cost twice as much?

The answer usually has very little to do with the accounting itself. The difference is almost always structural. It comes down to how the firm behind the accounting is built.

Brand Spend Gets Passed to You

Some administrators operate with large marketing machines behind them. They sponsor conferences, maintain large sales teams, and invest heavily in industry visibility.

Brand recognition has real value, particularly with institutional allocators who like to see familiar names on the service provider list. But those investments become part of the firm's cost structure. In practice, managers are often paying not just for accounting services, but for the marketing infrastructure surrounding the firm.

Location and Compensation Structures Matter More Than You Think

Many administrators rely heavily on staff in the most expensive financial centers in the world. Office footprints, staffing hierarchies, and compensation expectations in those markets create a certain baseline cost, one that gets embedded in the fees charged to managers.

Talent is essential in fund administration. But how a firm organizes and compensates its workforce has a meaningful impact on the economics of everything downstream.

Technology Is the Real Dividing Line

This is the one that matters most.

A large portion of the industry still depends on third-party accounting platforms as the backbone of their operations. These systems can be useful tools, but they impose real limitations. When an administrator doesn't control the accounting system itself, it becomes difficult to redesign workflows or embed automation directly into the accounting logic.

Technology ends up sitting around the accounting system rather than inside it.

As a result, many firms build additional software layers on top, onboarding portals, reporting dashboards, document platforms, that create the appearance of modern infrastructure. But behind the interface, a surprising amount of work may still be manual.

A common example: if the onboarding system isn't directly integrated with the accounting platform, investor data often has to be transferred into the books manually. That friction requires people to resolve it. And when operational processes depend on people resolving friction, costs scale with headcount.

What Changes When Automation Is Actually Embedded

For decades the industry accepted the headcount model as normal. As funds grew, administrators simply hired more accountants.

AI is beginning to change that dynamic, but only when automation is embedded directly into the accounting system itself, not layered on top of it.

When capital call data enters an integrated system, the ledger can automatically generate the related investor allocations, update capital accounts, and prepare the associated reporting, without a person reconstructing those entries manually. The same logic applies to management fee calculations, performance allocations, and reconciliation workflows.

None of this eliminates the need for experienced professionals. Fund accounting still requires judgment and oversight. What changes is how those professionals spend their time. Instead of constructing entries manually or moving data between systems, accountants supervise systems that perform those tasks.

Over time, that changes the cost structure of the entire operation. Funds can scale without requiring the same linear growth in operational staff that historically defined the industry.

The Brand Premium, What It Actually Costs

Many managers raise a familiar counterargument: institutional investors prefer certain administrators. The comfort of a recognizable name carries signaling value with LPs.

That dynamic is real. But it raises a practical question.

How much is that signaling premium actually worth?

If an administrator costs $150,000 a year more than an equally capable alternative, that difference compounds over the life of the fund. Over ten years, the premium may approach $1.5 million, capital that ultimately belongs to LPs.

At some point, the signaling value of a brand name has to be weighed against the drag it creates on investor returns.

The Mismatch Problem Nobody Talks About

Many mid-sized funds choose the largest administrators in the market. The logic is understandable: recognizable brands, enormous client rosters.

But that can create a quiet mismatch.

Consider a $500 million fund working with an administrator whose typical clients manage $5 to $10 billion. That fund represents a small relationship inside a very large client base.

Large organizations naturally devote the greatest attention to their largest relationships. That's simply how service businesses operate.

Many managers find that working with an administrator where their fund represents a meaningful client relationship leads to closer engagement and more direct access to senior teams.

The Question Worth Asking

When evaluating fund administrators, managers often focus on service teams, references, and reporting samples. Those factors matter.

But the more revealing question is structural: How is the administrator actually built?

Brand spending, compensation structures, and technology ownership all shape the economics of the firm providing the service. Those structural decisions ultimately determine where pricing sits, and whether it's likely to move over time.

Which brings us back to the original question.

If the output is accounting, is it really worth to pay twice as much for it?

About the Author

Shalin Madan is co-founder of Formidium and former hedge fund manager with 25 years in alternative investments and fund administration. At Formidium, proprietary technology supports over $34 billion in AUA, delivering institutional-grade capabilities with boutique-level service for real estate, private equity, venture capital, and digital asset funds.